Last week we went through how revenue management can use the displacement calculation with many examples where in most of them at first thought it seemed to be good business and generating more revenue, however it is obvious to say that hoteliers have various costs associated with everything including room, F&B , …..etc. However, there are different types of costs that are important for hoteliers to understand, because they impact results in different ways, and this where to address the displacement analysis.

Displacement Analysis

Since hotels have a fixed capacity, whenever they sell a room, they are taking a chance that they might be taking rooms out of inventory (Overbooking) that could be requested later at a higher rate but one of the Revenue Management purposes is to keep this action from happening.

Groups Displacement Analysis

Moving to the displacement analysis is more complicated than the calculation, but that would be easier for revenue management. Having done the basic displacement calculation for groups and individuals, let us go for more details with the groups. It shows in the discussed group scenario that we have the tendency to accept group B, because it generates more revenue, but before you decide, go back to the above mentioned questions and add the below for more consideration:

- What is the fixed room cost for the group?

- What are the meals, meeting cost for the group?

- What are the No show and cancellation conditions for the group?

- What is the hotel free room and upgrade policy for the group?

- What is the early check in and late checkout charges policy for the group?

- What other charges policy for the group i.e. parking, internet, portal fees…etc ?

- How the group will affect the pre and post days.

- As many hoteliers do since the group is generating high value of revenue , What other free benefits you offers t o the group. i.e. free internet, free parking, free late check out, free portal services, free cancellation and no show…etc.

The more questions you have, the more clear the picture becomes and you can make better decisions. Detailed analysis can help for each revenue area considering the fixed room cost per night; what do you think it will look like?

Be the first to know, sign up here and stay up to date with our latest revenue management news, updates and special offers

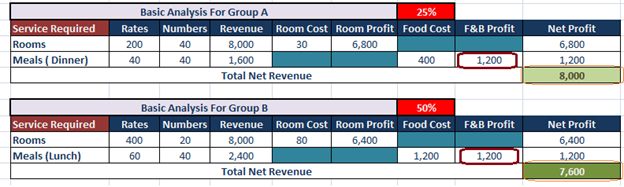

F&B: In our groups scenario let’s say Group 1 joining the dinner buffet at a food cost of 25% and Group 2 has a cost of 50% for their lunch. Both would contribute the same amount of revenue! ($1,200)

Rooms: Assume that Group 1 takes only standard rooms at a lower rate ($200), but also with a lower fixed room cost of $30 a night and Group 2 books only suites ($400), which have a fixed room cost of $80 per night.

With the Displacement analysis Group 2 became less interesting with less revenue / profit distribution. As you can see with the last scenario Group 2 went from our ‘favorite’ business as an equal with Group 1 to less ‘favorite’, because of the costs and displacement analysis we have done.

Groups and transients Displacement Analysis

Part of the process of analyzing the value of a group is to perform a solid displacement analysis. A displacement compares the value of different pieces of business to identify the one that brings the most value to the hotel.

A group displacement analysis is the process of analyzing group business based on the total value of the business and comparing it to the total value of the transient business that would be displaced if the group business was accepted. The group value includes all food and beverage spending, meeting room rental and any additional outlet spending, minus any costs involved.

With groups, it is usually worthwhile to do a displacement analysis, where we look at history to determine how many rooms from higher rated segments (usually Transient Rack and BAR ) are usually sold on these days of the week during this season. Then, after the group business is added determine if there is any demand that cannot be accommodated. In other words, is the hotel going to be full and so some of the last people to book will be turned away or those booking will be rejected. Multiply the number of guest rooms that will be denied times the average rate for that segment of business. If that is higher than the group revenue, then the group should be turned away. Obviously, if the profit from the ancillary in-house revenue from the group is higher than the profit from the ancillary revenue of the transient guests, then that has to also be factored into the decision.

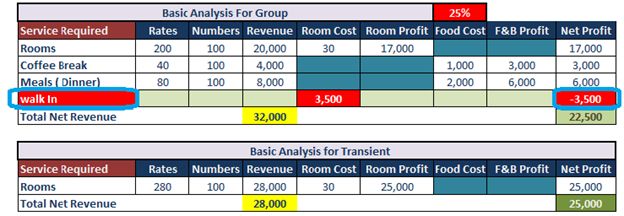

The following is an example of a simplified displacement analysis. It compares a potential group’s business to the transient displacement that would occur if the group was accepted at the current values.

The example above is simplified to provide a value comparison between group and transient business. It does not take into consideration transient length of stay and the impact that group acceptance will have on demand for room nights before and after the group block.

At first glance, it appears that the group would not be profitable because the room revenue from the transient business brings in $8,000 more than the group business.

However, when the ancillary revenues are added, as well as the costs associated with both pieces of business, it turns out that the group is more valuable to the hotel by $1,000. If an analysis indicates the group is not profitable and it is best not to accept the group, the hotel should consider offering alternate dates to the group. Dates with less transient demand will result in a more positive impact from the group. Another option that will increase the value of the group is to increase the rate offered. If you increase the rate and revise the analysis, the overall group value will increase.

But is a situation where “walking” would apply by the hotel, that must also be considered in the calculation, as this is considered a cost, see the below example.

When the possibility of “walking” is calculated into the equation, the group is no longer profitable for the hotel. Another element that should be included in the displacement analysis is the booking method.

Knowing the occupancy rates for your facility and services, including the number of guests you turn away because no rooms are available, helps you determine what mix of negotiated and transient rooms will maximize revenue for your hotel.

Understanding Cost

The purpose of understanding the costs of an occupied room is to allow hoteliers to understand the expenses per occupied room and being able to identify and understand the expenses per occupied room provides hoteliers with an opportunity to not only control expenses but also to identify any trends that may be impacting business.

Part of understanding the costs associated with occupying a room, and thus understanding the profitability potential, is to understand the difference between a fixed cost and a variable cost.

A- Fixed cost is the cost associated with an occupied room regardless of the total number of rooms occupied. Hotels will incur costs that require a certain level of staffing at the front office such as the front desk, phone operators and bell staff regardless of how many rooms are occupied on a given night. These costs are incurred when the hotel opens its doors and operate regardless of the number of rooms occupied.

B- Variable cost is the additional cost that will be incurred when additional rooms are sold. A variable cost will change and is dependent on the total number of additional rooms sold. An example of a variable cost is an additional housekeeper that will be scheduled to work only after a certain number of rooms are sold.

In addition to the displacement analysis there are of course other elements that must be considered above and beyond being able to compare the numbers. Some of the other considerations are listed below.

- Another piece of the puzzle that may be important to consider for some pieces of group business is the long term potential that this group may bring to the hotel. Will this piece of business bring additional group or transient opportunities? If so, when do we expect them? Will they be during peak demand dates when the hotel does not need the business, or will they be during slower times when the hotel needs the business? This needs to be weighted accordingly.

- Is this a regular event that the hotel wishes to capture?

- Is there known history to this group?

- Are there any other potential ancillary revenues that may be realized through this group?

- Does this piece of business bring any political advantages to the hotel?

- Is this a significant customer of the hotel company and thus, shouldn’t the customer’s overall value to the entire corporation be considered?

These are a few considerations that may or may not apply to the decision process. If they are applicable to a hotel or a specific piece of group business, then they should be considered and weighted accordingly.

By combining the scientific analysis with human judgment, hotels can optimize the group side of the revenue equation and move toward a total hotel approach to revenue management.

The final step in accepting or rejecting a piece of group business is to follow up on the decisions and measure the results. This will help the hotel enhance decisions in the future and learn from any mistakes or oversights.